In Oil & Companies News 07/02/2017

Donald Trump and global crude producers are set to take prices on a bumpy ride this year, according to the world’s biggest independent oil trader.

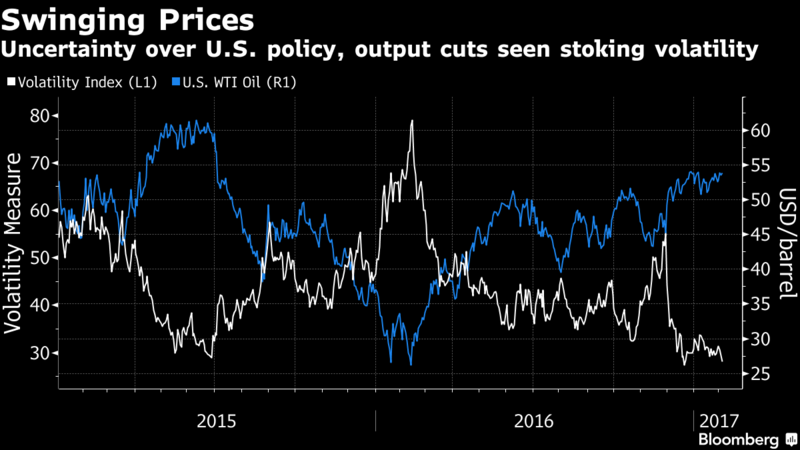

As investors are kept on tenterhooks over U.S. policies and whether OPEC and other nations will curb output as pledged, global benchmark Brent crude may vacillate between $52 and $62 a barrel, according to Kho Hui Meng, the head of the Asian arm of Vitol Group. The market’s structure could also shift in the third quarter, with near-term cargoes turning costlier than those for later delivery, flipping from the other way around.

“I think this market is going to be very volatile,” Kho, the president of Vitol Asia Pte., said in an interview in Singapore. “People are worrying about U.S. policy. With the new administration, a lot of things are being speculated. So we can’t predict the future, we just have to wait.”

The sentiment reflects the uncertainty gripping markets amid Trump’s ascent, with traders of everything from currencies to metals and stocks trying to decipher the effects of measures by the leader of the world’s biggest economy. The oil market has been ruffled by the prospect of more geopolitical tensions on his harder line on major producer Iran. He’s also mooted a border tax on imports, which Goldman Sachs Group Inc. says had a low chance of being introduced but could trigger an oil selloff if implemented.

Trading companies such as Vitol and rivals including Trafigura Group and Glencore Plc could reap rewards from volatility. Vitol’s $1.6 billion in earnings in 2015 were boosted as it profited from price swings in the energy market. It posted a 42 percent decline in first-half 2016 profit amid fewer opportunities to benefit from price changes.

The company, which is formally incorporated in Rotterdam but operates from locations including Geneva, London, Singapore and Houston, has experienced strong growth over the last 20 years on the back of expanding oil trade, large price swings and, more recently, investment in storage and refining. In 1995, Vitol earned just a little over $20 million.

Oil traders often look to take advantage of a market structure known as contango — where future prices are higher than current levels, allowing investors to buy oil cheap, store it in tanks or ships and lock in a profit for a later sale. But with global producers cutting output, the market may be poised to go into backwardation, when prompt crude is costlier than later cargoes.

The structure is now “quite flat so people are still watching,” Vitol’s Kho said. “Once the backwardation comes in, which we’re not there yet, then people begin to look at the viability of the floating storages and ultimately they’ll come out.”

Output Curbs

Oil has fluctuated above $50 a barrel since a December deal between the Organization of Petroleum Exporting Countries and other producers to trim supply by as much as 1.8 million barrels a day to ease a global glut. While OPEC members including Saudi Arabia are implementing their share of cuts and Russia says it’s ahead of schedule on its reduction, investors are wary of America pumping more. The revival of U.S. drilling has entered into its ninth month, extending the biggest surge of oil rigs in more than four years.

Brent for April settlement was little changed at $56.80 a barrel on the ICE Futures Europe exchange by 12:51 p.m. London time. U.S. benchmark West Texas Intermediate for March delivery was up 8 cents at $53.91 on the New York Mercantile Exchange.

“People also recognize that as oil tightens up and the price begins to rise, shale oil in the U.S. will start to come out again,” Kho said. “We’re seeing signs of that but it isn’t overwhelming yet.”

With a majority of the output reductions coming from Middle East nations, the regional Dubai crude benchmark has turned costlier than WTI and strengthened relative to Brent. That’s opened the window for arbitrage cargoes to flow into Asia from regions including the North Sea and West Africa.

While the stream of such oil from the U.S. and Europe to Asia won’t probably be the norm, it will continue to be an opportunistic trade in 2017, Kho said. Middle Eastern crude will remain the “base flow” for Asian refiners, in addition to West African supplies. Shipments from the U.S. and North Sea may not be as common going forward as the arbitrage window can open and close with market volatility, he said.

In the world of fuels, the lack of new large-scale refineries coming online globally in the near term could tighten the market for distilled products, Kho said. That’s especially pertinent to diesel, which makes up the biggest portion of output from processing units.

“Diesel has gone through a rough time for a number of years, but probably will turn to come back,” said Kho. This would strengthen the spread between diesel and fuel oil, ahead of the implementation of new International Maritime Organization standards that could spur ships to switch to cleaner products such as ultra-low-sulfur diesel. Oil-product markets are currently in a “sweet spot,” backed by seasonal winter demand and refinery outages, according to Kho.

The direction of the crude market, meanwhile, may hinge on the effects of the Trump administration’s policies.

Investors and traders are “waiting for a signal from the U.S. because this is the biggest equation unknown,” Kho said. “It’s the function of the global economy. If there’s nothing drastic from the U.S., it will be quite good this year.”

Source: Bloomberg